Every year, thousands of Southern California homeowners from Newport Beach to San Bernardino discover a harsh reality: their water damage insurance claim has been denied or severely underpaid. The rejection letter arrives filled with terms like “gradual damage,” “maintenance issue,” or “flood exclusion” – language that devastates families already dealing with damaged homes. What insurance companies won’t advertise is that California water damage policies contain carefully crafted exclusions that leave property owners vulnerable precisely when they need coverage most. Understanding these hidden gaps before disaster strikes can mean the difference between full restoration and financial ruin.

The Gradual Damage Trap: California’s Most Expensive Exclusion

Insurance companies in California have perfected the art of denying claims through the “gradual damage” exclusion, a provision that affects countless homeowners across Los Angeles County and Orange County. This exclusion states that damage occurring over time – even just 14 days in some policies – isn’t covered. Yet California’s unique climate creates situations where sudden events cause gradual manifestation. A pipe might crack during an earthquake, but the leak remains hidden behind stucco for weeks. Santa Ana winds might drive rain through microscopic gaps, with damage appearing months later. By the time homeowners discover the problem, insurers classify it as gradual, leaving property owners to foot massive restoration bills.

The particularly cruel aspect of this exclusion emerges in California’s Mediterranean climate zones. Our sporadic rainfall means water intrusion often goes undetected during long dry spells. Properties in coastal areas like Huntington Beach face salt air corrosion that weakens plumbing systems imperceptibly until catastrophic failure occurs. Professional water damage documentation from companies like Superior Restore becomes crucial in these cases, as we can often demonstrate through moisture mapping and thermal imaging that seemingly gradual damage originated from a specific, covered event. Without this professional evidence, insurers routinely deny claims worth tens of thousands of dollars.

The Earthquake Loophole That Bankrupts Homeowners

Here’s what insurance companies operating in seismically active Southern California deliberately obscure: standard homeowners policies exclude damage from “earth movement,” but the resulting water damage gets caught in coverage limbo. When the Ridgecrest earthquakes struck in 2019, hundreds of Riverside County and San Bernardino County homeowners discovered broken pipes days or weeks later. Their earthquake insurance covered structural damage, but most policies excluded the subsequent water damage. Their homeowners insurance denied claims because the initial cause was earth movement. This coverage gap, unique to earthquake-prone regions, has left California families with restoration bills exceeding $100,000.

The complexity multiplies with California’s specific soil conditions. Expansive clay soils throughout the Inland Empire shift dramatically between wet and dry seasons, stressing plumbing systems in ways that blur the line between earthquake damage and soil movement. Insurance adjusters exploit this ambiguity, arguing that pipe failures result from long-term soil pressure rather than seismic events. FEMA’s earthquake preparedness guidelines acknowledge these vulnerabilities, yet insurance policies haven’t evolved to address California’s unique geological risks.

The “Flood” Definition Scam in Desert Communities

Insurance companies know that most California homeowners don’t understand the critical distinction between water damage and flood damage. In insurance terms, “flood” means water that touches the ground before entering your home – even if it’s just pooling on your patio. During atmospheric river events, when wind-driven rain accumulates against French doors in Laguna Beach or pools on flat roofs in Palm Springs, insurers invoke the flood exclusion. Your homeowners policy won’t cover it, and without separate flood insurance, you’re completely exposed. The cruel irony? Many Southern California communities aren’t in designated flood zones, so homeowners never thought to purchase flood coverage for their hillside or desert properties.

This definition particularly devastates owners of Spanish-style homes common throughout Orange County and San Diego County. These architectural designs, with their courtyards and low-threshold entries, funnel rainwater in ways that technically qualify as “surface water” under insurance definitions. A clogged courtyard drain during a brief but intense storm transforms covered water damage into excluded flood damage. Superior Restore’s Mission Viejo team regularly assists homeowners in documenting the precise water source to challenge these denials, but without professional intervention, claims are routinely rejected.

The Slab Leak Shell Game: Coverage Today, Gone Tomorrow

California leads the nation in slab leak incidents due to our unique combination of expansive soils, seismic activity, and aging copper pipes. Yet insurance companies have systematically removed or limited slab leak coverage, often through policy endorsement changes that homeowners overlook. Many policies now cover only the water damage from slab leaks, not the cost of accessing or repairing the pipe itself – which can exceed $20,000 in Southern California homes. Worse, after one slab leak claim, insurers frequently add exclusions or drop coverage entirely, leaving homeowners vulnerable to future incidents in a state where multiple slab leaks are common.

The insurance industry’s response to California’s slab leak epidemic reveals calculated risk transfer to homeowners. Companies use predictive modeling showing that homes in certain zip codes across Riverside County and Los Angeles County have a 40% chance of experiencing slab leaks within 20 years. Rather than pricing this risk appropriately, they’ve chosen to exclude it, knowing that most homeowners won’t discover the limitation until they file a claim. The particularly insidious aspect? Insurers often approve initial emergency water extraction but deny the actual repair costs, leaving homeowners with torn-up floors and no coverage for restoration.

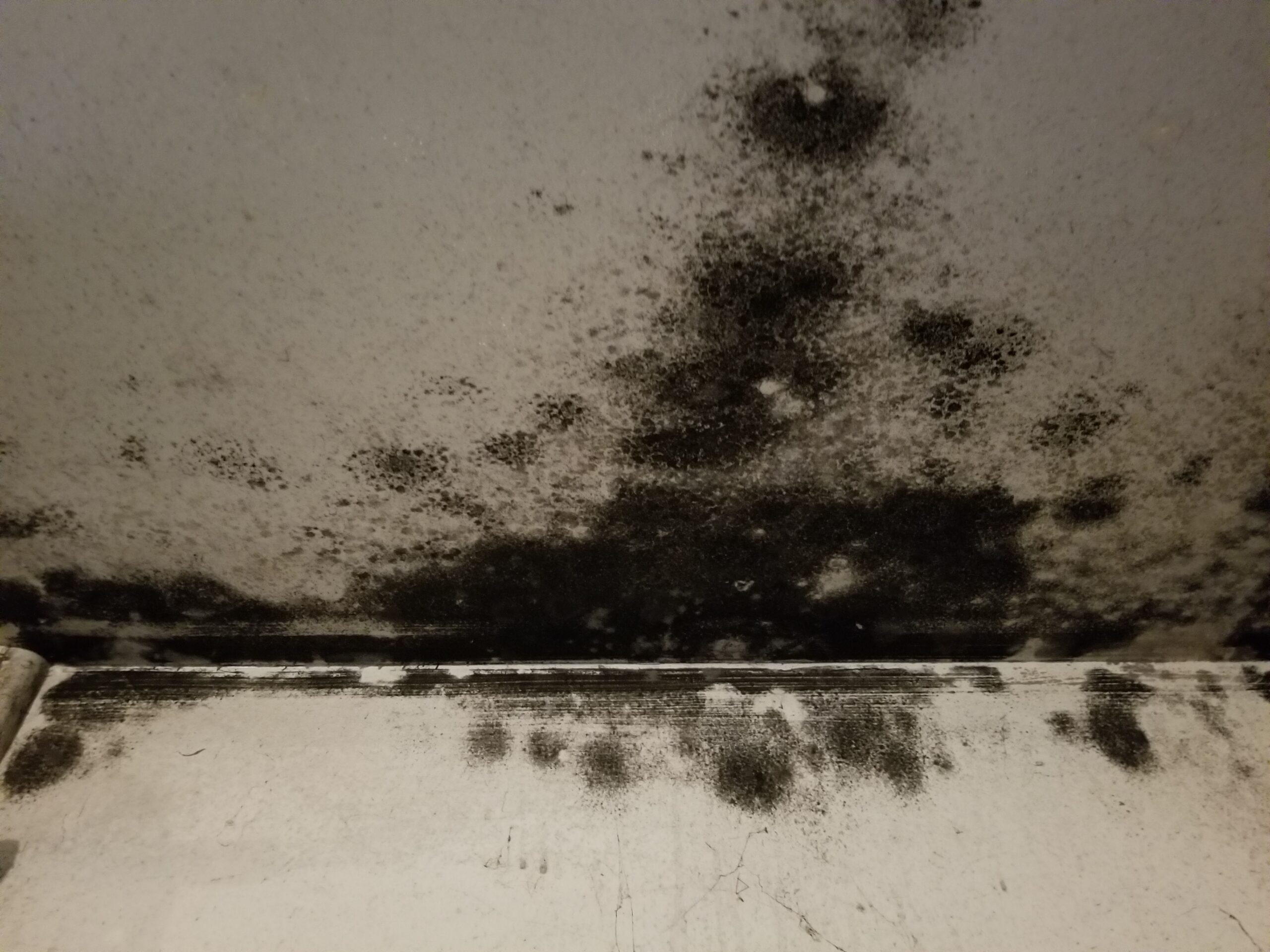

The Mold Coverage Disappearing Act

Following California’s toxic mold litigation boom in the early 2000s, insurance companies quietly revolutionized their policies to eliminate or severely cap mold coverage. Most California homeowners policies now limit mold damage to $5,000 to $10,000 – a fraction of actual remediation costs in our warm, humid coastal zones. The California Department of Public Health’s mold guidelines recommend extensive remediation protocols that routinely cost $20,000 or more, yet insurance coverage hasn’t kept pace with these health-based standards. The gap between coverage and actual costs devastates families, particularly in moisture-prone areas from San Diego’s marine layer zone to San Francisco Bay Area microclimates.

Insurance companies exploit California’s complex mold disclosure laws to further limit coverage. They argue that if mold wasn’t discovered and remediated within their arbitrary timeframes – often as short as 72 hours after water damage – it becomes a maintenance issue rather than a covered peril. This timeline ignores the reality of hidden mold growth within wall cavities and under flooring, particularly in Southern California’s predominant slab-on-grade construction where moisture can persist undetected for weeks.

Superior Restore: Your Advocate Against Insurance Denial Tactics

When insurance companies deploy these coverage traps against California homeowners, Superior Restore’s comprehensive documentation and restoration expertise levels the playing field. Our IICRC-certified technicians understand exactly how insurers interpret policy language and what evidence overcomes common denial tactics. We create detailed photographic documentation, moisture maps, and chain-of-causation reports that challenge gradual damage exclusions. Our thermal imaging proves hidden damage originated from covered perils, not long-term maintenance issues. Most critically, we work directly with insurance companies throughout Southern California, speaking their language while advocating for maximum coverage. Don’t let insurance company tactics leave you paying for water damage that should be covered. Contact Superior Restore immediately at the first sign of water damage – our 24/7 emergency response team not only minimizes damage but also preserves the evidence needed to secure your rightful coverage. From the initial call through final restoration, we fight to ensure insurance companies honor their obligations to California policyholders.